One of the most critical challenges facing Britain’s Labour government is how to promote business investment while still protecting consumers.

On one hand, Labour wants to promote economic growth and this requires a significant increase in investment, which in turn means Britain has to become a more attractive destination for investors, including by reducing regulatory burdens on them.

But on the other hand, the government was also elected on a manifesto promising tougher regulation to protect consumers in a wide range of sectors where companies were seen to have abused their freedoms, including water, energy, digital markets, transport, housing, health and social care.

Every government faces these competing pressures – to deregulate in order to drive investment, and to regulate in order to protect consumers – but the challenge is particularly acute for Labour today because of the inheritance it was handed when it was elected.

Stagnant productivity growth since the financial crisis means it is more important than ever to increase business investment, particularly in a world where international trade is subject to greater frictions. But at the same time, the dire fiscal position means there is less money to go round than when Labour was last in power, so it becomes more tempting to require businesses in play a bigger part in delivering policy objectives.

The trade-offs are real and cannot be wished away – but there are ways the government can deliver the maximum boost to investment at the lowest cost to consumers; and deliver the maximum protection for consumers at the lowest cost to investors.

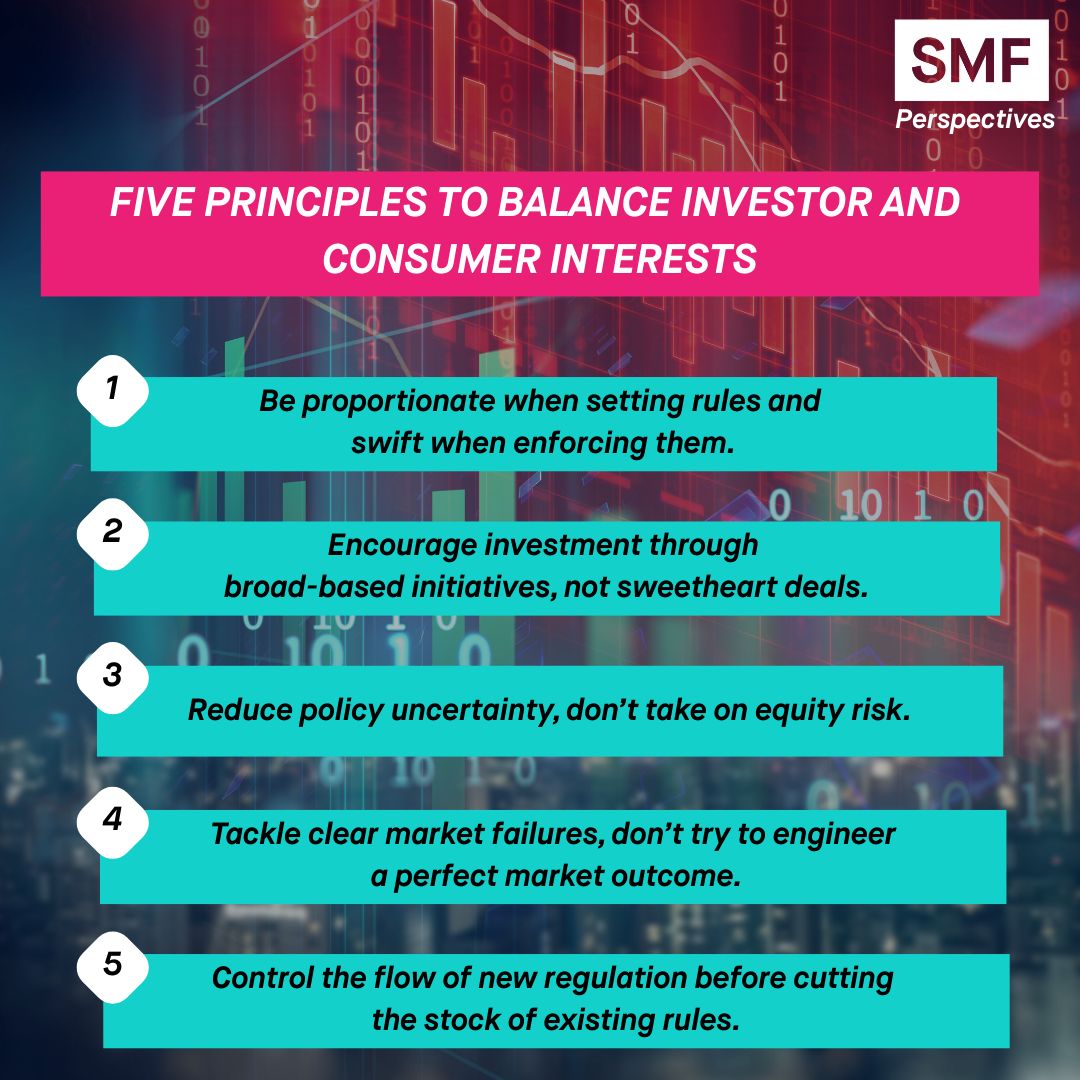

Here are five principles to follow:

-

- Be proportionate when setting rules and swift when enforcing them

- Encourage investment through broad-based incentives, not sweetheart deals

- Reduce policy uncertainty, don’t take on equity risk

- Tackle clear market failures, don’t try to engineer a perfect market outcome

- Control the flow of new regulation before cutting the stock of existing rules

1. Be proportionate when setting rules and swift when enforcing them

The co-founder of Deliveroo, Will Shu, was interviewed earlier this year following the announcement that the company was to be acquired by its American counterpart DoorDash. When asked about how the UK can make itself more attractive to companies and entrepreneurs, Shu said the following:

I don’t think it’s about taxes or anything like that. I think no one wants high taxes, but you don’t start a business because, you know, the tax rate, capital gains tax is 24 [per cent] versus 20…Ultimately, you want to start businesses because you believe in an idea and you have confidence that it can work, and there’s a system that is predictable and fair behind it. And I think predictability and fairness, that’s really what the government should strive for.

Like Shu, most business leaders recognise that governments will sometimes need to regulate or intervene in markets – but the way they go about it really matters. In Shu’s case, he was particularly burned by his experience dealing with the Competition and Markets Authority when it took over a year to review Amazon’s acquisition of a 16% stake in Deliveroo.

The example of the CMA is instructive. In recent years it gained a reputation for being particularly tough and interventionist in its merger investigations, which on the face of it seems odd given that the number of mergers it blocks each year is tiny (normally fewer than five deals or under 1 per cent of all the ones it reviews). But even where deals were ultimately cleared the process could be tortuous, for example a year in the case of Amazon/Deliveroo and 15 months in the case of Microsoft/Activision. Business leaders would often end up being surprised by which mergers the CMA decided to review, how long it took and how little feedback they were getting during the process. After Labour won the election in July last year, incoming ministers at the Treasury and the Business department found that the CMA was the regulator about which they received the most complaints from CEOs.

The easiest way for regulators to promote investment without any new legislation or extra money is by improving their processes so that they are more straightforward for businesses to deal with. For example, the government’s new strategic steer to the CMA emphasises that the Prime Minister wants to make the UK “a centre for certain, proportionate and transparent regulation” and that the CMA’s actions should be “swift, predictable, independent and proportionate.” These are clear priorities and the CMA chief executive has published a set of practical actions to improve the CMA’s “pace, proportionality, predictability and process”. For example, it set itself targets to reduce the length of its reviews while offering greater senior engagement to the companies concerned. Other regulators could take a similar approach.

2. Encourage investment through broad-based incentives, not sweetheart deals

The ONS tracks levels of business investment in the UK, with the latest release showing that it increased by 3.9 per cent in Q1 2025 and that it is 6.1 per cent above the level in the same quarter a year ago.

However, media and political attention tends to focus less on the overall statistics than on individual announcements of investments that are being planned or canned. This naturally create a temptation for the government to negotiate with individual companies to encourage them to invest in the UK, and potentially to offer something in return.

But there is a problem here. What is good for an individual investor is not necessarily good for investment across the economy as a whole. For example, Chris Hohn, founder of the hedge fund TCI, was recently interviewed on Nicolai Tangen’s In Good Company podcast. Hohn was asked what makes a good investment and he replied that the most important thing is “high barriers to entry”. The reason Hohn gave was that “competition kills profits” whereas without competition the company can “price above inflation” and enjoy sustainable and predictable earning power.

From the perspective of an investor contemplating an acquisition in isolation, that makes total sense. Often it is the existence of a market failure – like a monopoly or high customer switching costs – that makes a particular investment opportunity look attractive. But if the economy as a whole was characterised by such market failures, with high barriers to entry and companies pricing above inflation, it would be disastrous both for investment and for consumers. There would be a one-off inflow of capital as investors sought to acquire these attractive and low-risk cash flows, but they would then have very little incentive to invest or innovate further, while at the same time customers would end up paying over the odds and with no ability to switch elsewhere.

Furthermore, when governments start cutting deals with individual investors, they face several risks. Political decisions are at high risk of being influenced by lobbying, so we may end up with the investment projects that are the most favoured by powerful political interests rather than those which would generate the biggest returns. That is why governments have such poor records historically when it comes to ‘picking winners’. Businesses could also exploit their information asymmetry with government to request a subsidy or a policy change in return for an investment that they were planning to make anyway, so there is a possible deadweight loss. It is even possible that a government’s willingness to cut deals could lead to less investment, as companies hold back possible investments to use as bargaining chips for when they need something from the government.

Instead, policies to encourage investment should be broad-based and enable multiple companies to take advantage of them, rather than relying on the government to cut deals with individual firms. There is no shortage of ideas here. Research has pointed to number of specific areas where the UK government or devolved administrations could take action in ways that would promote , from transport infrastructure improvements in major non-London conurbations to regional distribution of public support for R&D. John Kingman has explored a number of these, several of which would have a particularly strong impact on growth outside London, including transport capital projects like the Transpennine upgrade, an expansion of city devolution and a more sustainable university funding model. And the venture capitalist Ian Hogarth has shown where Europe needs to focus in order to be a better home for growing tech companies, by making it easier to start businesses and spin them out of universities and by reforming corporate governance to help companies stay independent for longer by allowing founders to resist short-term investor pressure to sell early.

If the government cuts a deal with a single investor, it gets one investment. But if it makes a policy change that applies generally, there is no limit to the number of investors that can take advantage of it.

3. Reduce policy uncertainty, don’t take on equity risk

One point that investors rightly make to the government is about the importance of certainty. But it is critical to remember the distinction in finance between uncertainty and risk. Governments should try to reduce the former without taking on more of the latter than is necessary.

In particular, governments should seek to reduce the kind of needless uncertainty over future policy which makes it hard for investors to make decisions. This is especially important for long term investments, for example in infrastructure, where investors are taking on risk now but might only see the returns over many years. In these cases politicians might initially promise a pro-business regulatory regime in order to attract the investment, but investors worry that once they have parted with their cash, politicians will intervene, change the rules and expropriate the returns. (It is what economists call a ‘time inconsistency’ problem.) This is why, for all the failures of regulators such as Ofwat, there is merit in keeping utility price controls out of direct ministerial control so that investors can have confidence that once they have been set they will not be upended at short notice for political reasons. Ministers should get the overall regulatory framework right, as they are now seeking to do in water through the Cunliffe review, and they should give a strategic steer to the regulator on how it should approach its work, but having done so they should then avoid day-to-day interference and short-term policy changes.

But governments should not seek to eliminate the knowable, quantifiable and diversifiable risk that is a normal part of investment. In particular, they should avoid allowing risk to be transferred to the taxpayer, while the investor gets the return. And if they are going to guarantee a return, it should be a modest one that takes into account the transfer of risk.

We saw this problem in the financial sector before the global crash. The banks were perceived as being too big to fail so they were able to borrow at low rates because of an implicit government guarantee. This meant they made bigger profits in the good times which in turn encouraged them to take bigger risks, which made a crisis more likely, for which taxpayers then had to foot the bill. That is why since the crash the Bank of England has put in place measures such as the Special Resolution Regime (SRR) to enable banks to fail in an orderly way without relying on a taxpayer bailout, and this was used successfully in 2023 in the collapse of Silicon Valley Bank. In the water sector, where Thames Water is on the brink of financial failure, there exists a Special Administration Regime (SAR) which can allow a poorly performing or insolvent company to fail safely.

4. Tackle identifiable market failures, don’t seek to engineer a perfect market outcome

In order to decide whether a given market needs more regulation, we must have a clear and realistic view of what the market can and should be delivering. There are some things that markets are good at and some things they are not very good at.

When they work well, markets are very good at processing information and providing incentives. If a good is in short supply relative to demand, the price of that good will rise, incentivising existing players to increase production, new entrants to come into the market, and new and existing players to innovate.

Sometimes there is a failure which makes it harder for the market to do this job effectively. These market failures can include monopoly (where a company has enough market power that it can raise prices without worrying about competition), externalities (where the actions of a company impose costs on third parties or wider society, for example pollution) or information asymmetries (where a company can use its superior knowledge of a product or a customer to take advantage). This is where regulators are well-placed to step in, for example by removing barriers to entry or giving customers access to better and clearer information. Once the market failure has been addressed, the market can then be allowed to get on with its job of processing the information and providing the incentives.

But there are some things that markets don’t tend to be very good at, such as generating fair or equal outcomes. To take an obvious example, the labour market tends to lead premiership footballers to be paid a lot more than shop workers, not because the differential is fair objectively but because of the supply and demand for their respective labour. Policymakers generally think that the solution to the unfairness is not to intervene in the labour market so that footballers and shopworkers are legally required to be paid the same, but instead that once the labour market has done its job of balancing supply and demand, there should be a system of progressive taxation to address the unfairness. Elsewhere, policymakers might well conclude that it is unfair that people on low incomes have to pay so much for their energy or housing but imposing price caps or rent controls is unlikely to help because it will blunt the price signals, divert investment elsewhere and lead to shortages of the very things that policymakers want to see more of.

This all happens because market competition is fundamentally a discovery process, providing information and incentives to balance supply and demand. The whole point is that the ‘correct’ price or number of players cannot be known in advance. This is especially the case in new and fast-developing markets such as in artificial intelligence where politicians cannot possibly predict with confidence what the end point would or should be. Rather than seeking to engineer precise market outcomes, it is far better for the government and regulators to address the underlying causes of why prices are so high or quality is so low – for example planning restrictions in housing, a lack of cheap baseload energy or shortages of certain workers – and then allow the process of market competition to work. This does not mean that greater equality is an inappropriate objective for the government to aim at. Far from it. But as a general rule, politicians are better off addressing the underlying market failures so that the market to work effectively, and then addressing inequality through redistribution in the tax and benefit systems, rather than intervening on an ongoing basis in individual markets to try and make them deliver the ‘right’ or fair outcome.

5. Control the flow of new regulation before cutting the stock of existing rules

Political debates on regulation tend to assume that consumers want more regulation and businesses want less; and that the reason businesses want less is that regulation is costly to implement. That is why deregulatory initiatives tend to be called things like “red tape challenge” or “bonfire of quangos”, and you can read more about their mixed history of success here.

But in my experience the biggest worry for business leaders, especially of bigger businesses, is not so much the burden of complying with existing regulations. If a business is active in the UK market, it is true that it might wish some regulations had not been introduced. But by now those rules are in force and the company has probably put compliance systems in place. Indeed, in some cases, these may constitute a barrier to entry against potential competitors, so firms might on balance prefer to keep existing regulations even if they add to their cost base.

First, to help investors, the government should put a greater priority on controlling the flow of new regulation than on cutting the stock of existing regulation. It helps that this should also be more manageable politically. Getting rid of an existing regulation often means confronting a group of vested interests that have grown up in support of that rule. Plus, as mentioned above, incumbent businesses may well not be desperate to remove it if by now they are successfully complying with it. By contrast, when a putative regulation is still just an idea, that alliance of lobbyists and vested interests tends to be weaker. The best time to get rid of an unwarranted regulation is before it has been introduced.

As a next step, therefore, when elected politicians are presented with demands for a new regulation, either from their constituents or from vested interests, they need better to evaluate the pros and cons. This is not about the kind of quantitative cost-benefit analysis that is conducted by a government department, often the very department that may be a pushing a new regulation. Instead, the CMA or the new Regulatory Innovation Office could be given a specific role to advise publicly on new regulatory proposals. They would be asked to address some straightforward questions: Is there clear evidence of a market failure? What might the (intended and unintended) consequences of the proposed regulation be? Are there alternative proposals that should be considered? And the CMA/RIO would be asked to answer these questions in an objective and non-technical way to help public and parliamentary debate. When a new regulation is proposed, a sympathetic politician need not therefore call for it to be passed straight away but rather for an immediate report from the CMA/RIO and for parliamentary time to be allocated to debate it. This would allow for a much more informed and effective public and political discussion, with a counterbalance to some of the vested interest lobbying.

Additionally, where the government wants to protect consumers from unfair business behaviour, it should check that it is enforcing existing regulations before it starts creating new ones. And this should be more feasible now that Parliament has strengthened consumer protection law through the Digital Markets, Competition and Consumers Act. This gives the CMA much stronger powers to impose penalties against companies that mislead consumers or treat them unfairly, and the CMA can take this action across any sector of the economy, so it should reduce the need for each sector regulator to create new rules which fulfil fundamentally the same purpose. This would also have the benefit that a cross-economy enforcer is less prone to capture by incumbents than a sector regulator.

Conclusion

A progressive government will always need to aim at both growth and fairness. It must not be forced into a binary choice between being “pro-investor” and “pro-consumer” but nor can it pretend that real policy trade-offs do not exist. That is why it is so important to find pro-investment policies that can be delivered at the lowest cost to consumers, and pro-consumer policies that can be delivered at the lowest cost to investors. The five principles in this essay are intended to be a guide to achieving that.

Stuart Hudson is a Senior Fellow at the SMF and a former Special Adviser to Gordon Brown and Senior Director of Strategy at the CMA. He is currently a Partner at Brunswick where he advises companies on regulatory issues.